The US–Iran conflict has triggered one of the largest energy supply shocks in history by effectively closing the Strait of Hormuz and interrupting around one-fifth of global oil and LNG trade flows. Consequently, Brent crude prices surged to a peak of USD 118 per barrel before retreating to below USD 80 per barrel in mid-June on emerging ceasefire signals. Global oil inventories have been depleting at a fast rate. Asia is particularly vulnerable to this major energy disruption, with around 80% of its crude oil and 90% of its LNG imports typically transiting through this critical chokepoint.

Across Asia, governments have responded with emergency measures not seen since the Covid-19 pandemic: fuel rationing, four-day work weeks, coal plant restarts, and record releases from strategic petroleum reserves. This raises the question of a persistent inflationary impact on Asia. This article discusses the consequences of the US-Iran conflict on advanced and emerging Asian economies and analyses the implications for inflation.

The immediate buffer against the supply shock has been the drawdown of strategic petroleum reserves across Asia. Japan and South Korea, which normally source 95% and 70% of their oil from the Middle East respectively, hold strategic reserves equivalent to approximately 30 weeks of supply. China, despite being the world’s largest crude oil importer, retains access to Iranian and Russian energy supplies via non-Hormuz routes and can switch electricity generation to domestic coal.

For most other Asian economies, the buffer is far thinner. India, Vietnam, Singapore, Bangladesh, Pakistan, and Sri Lanka hold limited strategic reserves of between 30 to 90 days. For the latter group, limited foreign exchange buffers and constrained fiscal space leave them exposed to a supply shock with limited policy tools to absorb the impact.

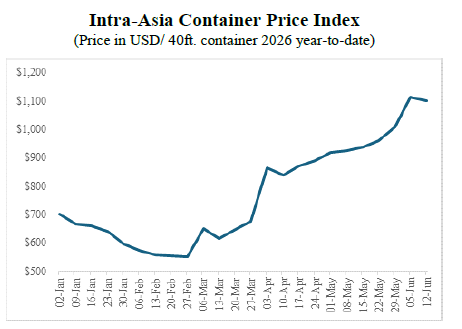

The inflationary consequences of the energy shock are transmitting through three distinct channels simultaneously. The first and most immediate is the direct pass-through of higher oil and gas prices into fuel, electricity, and transportation costs. This is already visible in container shipping costs, petrol queues, electricity surcharges, and airline fuel levies across the region.

The second channel operates through food and fertilizer prices. Disruptions to petrochemical supply chains have constrained the availability of LNG-derived fertilizer feedstocks, driving up agricultural input costs and threatening food security across South and Southeast Asia.

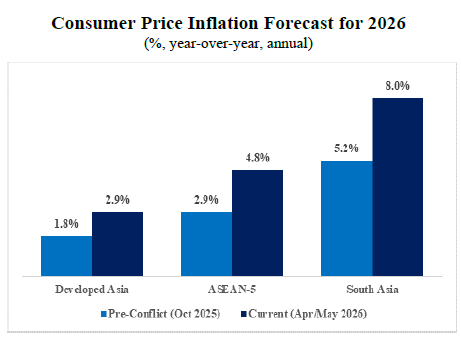

The third channel is currency depreciation: as Asian economies face surging energy import bills, trade balances have deteriorated and capital outflows have intensified, weakening currencies against the US dollar and amplifying import price inflation well beyond the direct energy component. These three channels are occurring simultaneously and aggravate its impact on regional inflation which is forecast to reach up to 5.2% for 2026, up from 3.0% in 2025.

Looking ahead, the announcement of an agreement offers a degree of cautious optimism. However, even a rapid resolution would not translate immediately into price and supply normalization. It is projected that it will take until early 2027 for production and trade patterns to return to pre-conflict levels across Asia, as clearing mines and logistics resumption from the Strait, restarting idled production fields could require months of sustained effort.

For most of Asia’s frontier and emerging economies, the damage to fiscal positions, foreign exchange reserves, and food security will outlast the conflict itself. Central banks across the region face a difficult balancing act between supporting weakening growth and containing inflation. The energy crisis in Asia will not be over when a deal is signed but rather when the region’s supply chains, reserves, and price levels have fully normalized.

Download the PDF version of this weekly commentary in English or عربي